The Capital One $425M Settlement 2025 remains unresolved after a federal judge declined to approve the proposed class-action agreement, delaying any payments to millions of customers while the parties return to negotiations over alleged losses tied to low-interest savings accounts.

Table of Contents

Capital One $425M Settlement 2025

| Key Fact | Detail |

|---|---|

| Proposed settlement value | $425 million |

| Status | Rejected by federal judge |

| Affected product | Capital One 360 Savings accounts |

| Eligibility window | September 2019 to mid-2025 |

| Payments issued | None as of late 2025 |

| Next step | Renegotiation or continued litigation |

Overview of the Case

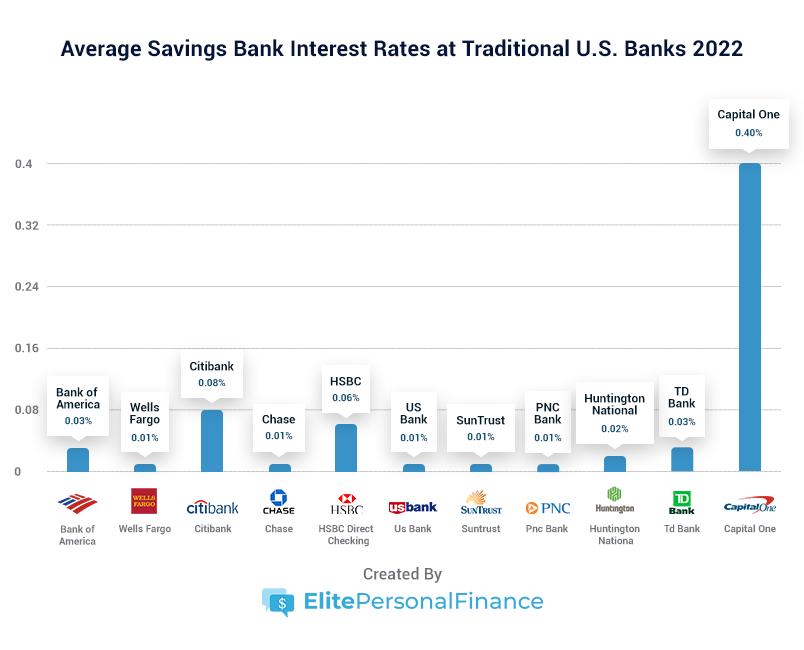

The lawsuit at the center of the Capital One $425M Settlement 2025 was filed on behalf of customers who held Capital One 360 Savings accounts, a legacy product that paid relatively low interest rates even as broader market rates climbed sharply.

Plaintiffs alleged that Capital One deliberately kept interest rates on these accounts depressed while aggressively marketing newer savings products that paid significantly higher yields. According to the complaint, the older accounts remained open and active, often holding substantial balances, despite offering returns far below prevailing market rates.

The case reflects a broader tension in modern consumer banking, where financial institutions manage multiple savings products simultaneously, sometimes with sharply different interest structures. Consumer advocates argue that this creates confusion, particularly for long-time customers who may assume their bank automatically adjusts rates in line with market conditions.

Capital One has consistently denied wrongdoing. In court filings, the company argued that it clearly disclosed account terms, gave customers the freedom to move funds between products, and never promised that rates on older accounts would match those offered on newer ones.

Who Would Have Been Eligible

Under the proposed settlement terms, eligibility would have included current and former holders of Capital One 360 Savings accounts between September 2019 and mid-2025.

The class definition covered customers regardless of whether their accounts remained open or had been closed during the eligibility period. This feature was particularly significant because many affected customers reportedly moved their funds only after learning of the rate disparity.

Customers holding Capital One’s newer 360 Performance Savings accounts were excluded. These accounts offered higher, variable interest rates that more closely tracked changes in the Federal Reserve’s benchmark rate.

Legal analysts note that the eligibility window was designed to capture the period during which interest rates rose rapidly following years of near-zero levels. During that time, some online savings accounts increased yields to more than 4 percent, while legacy products lagged far behind.

Why the Settlement Was Rejected

In late 2025, a federal judge declined to grant final approval to the $425 million settlement, concluding that it did not adequately compensate affected depositors relative to the scale of the alleged harm.

In the ruling, the court emphasized that the proposed payments represented only a fraction of the interest customers may have earned had their funds been held in higher-yield accounts. The judge also questioned whether the settlement sufficiently reflected the bank’s potential exposure if the case proceeded to trial.

The decision echoed growing judicial scrutiny of large consumer class-action settlements, particularly those involving financial institutions. Courts increasingly require detailed justification showing that settlement amounts fairly balance consumer losses, litigation risks, and legal fees.

The rejection effectively nullified all previously announced deadlines and paused the distribution process indefinitely.

What Payouts Might Have Looked Like

Although no final payment structure was approved, court filings provided insight into how compensation might have been calculated under the original proposal.

Payouts were expected to vary widely, depending on account balances, duration of ownership, and whether accounts remained open at the time of distribution. Customers with larger balances held over longer periods would likely have received higher payments.

Some customers would have received direct cash payments, while others might have received interest credits applied to active accounts. The settlement fund would also have covered legal fees, administrative costs, and service awards for named plaintiffs.

Consumer finance experts caution that even large-sounding settlements can translate into modest individual payouts once funds are divided among millions of account holders. This reality may have contributed to the judge’s conclusion that the agreement undervalued consumer losses.

Any revised settlement could introduce new payout formulas, minimum payment thresholds, or alternative compensation mechanisms.

Are Payments Being Issued Now?

No payments have been issued.

Because the court rejected the settlement, all previously announced deadlines — including those for selecting payment methods or opting out — are no longer valid. Customers should be wary of unsolicited emails or messages claiming that payments are imminent.

Consumer protection agencies routinely warn that high-profile settlement delays can attract scams, particularly when cases involve large numbers of potential claimants.

If a revised agreement is reached, customers would receive official notices by mail or email from a court-approved settlement administrator. Until then, no action is required.

What Happens Next

Negotiations between Capital One and plaintiffs’ attorneys are ongoing under court supervision. Legal experts say the parties face several possible paths forward.

One option is a revised settlement with a larger fund or restructured compensation model that addresses the court’s concerns. Another is continued litigation, which could involve additional discovery, expert testimony, and potentially a trial.

While trials in large banking cases are relatively rare, the possibility remains. A trial outcome could expose Capital One to significantly higher damages, though it would also carry risks for plaintiffs.

Capital One has stated publicly that it will continue to defend the case while engaging in court-directed discussions. The bank has not disclosed whether it is prepared to increase the settlement amount.

Broader Implications for the Banking Industry

The Capital One case highlights a growing regulatory and legal focus on so-called “product segmentation” in consumer banking. This practice involves offering different versions of similar accounts with varying features and rates.

Regulators have increasingly scrutinized whether such strategies unfairly disadvantage less active or less financially sophisticated customers. The Consumer Financial Protection Bureau has signaled interest in practices that may obscure meaningful rate comparisons.

Industry analysts say the case could influence how banks manage legacy products, particularly during periods of rapid interest rate changes. Some institutions have already consolidated older accounts or automatically transitioned customers to newer offerings.

What Customers Can Do Now

For affected customers, the most important step is staying informed through official channels. Maintaining records of account statements, balances, and communications with the bank may prove useful if a new settlement is approved.

Financial advisors also recommend that consumers regularly review savings account yields and compare them across institutions. Even small differences in interest rates can translate into substantial differences over time.

Customers who no longer bank with Capital One may still qualify for compensation if a revised settlement is approved, underscoring the importance of keeping contact information current.

Final Note

For now, the Capital One $425M Settlement 2025 remains unresolved, underscoring both the complexity of modern consumer banking disputes and the growing role of courts in evaluating whether large settlements truly serve the public interest.

As negotiations continue, millions of savers are left waiting for clarity on whether compensation will materialize — and whether future banking practices will change as a result.